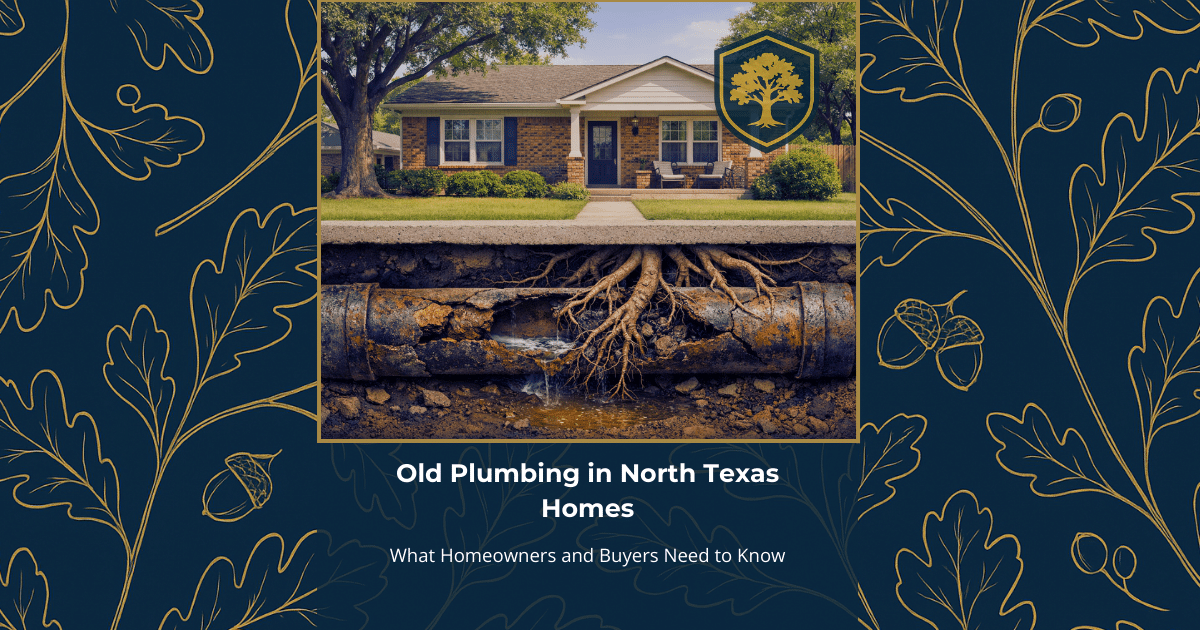

Old plumbing in North Texas homes is a common but often overlooked risk, especially in older Dallas–Fort Worth neighborhoods built decades ago. Many of these homes still rely on original plumbing materials, including cast iron sewer pipes, that naturally deteriorate over time beneath the slab.

As a result, sewer backups and plumbing-related insurance claims have become more common in older Texas homes. When problems occur, homeowners are often surprised to learn that homeowners insurance does not typically cover aging or deteriorated plumbing systems, even when interior damage is significant. Understanding how older plumbing fails and how water backup coverage works can help homeowners and buyers avoid costly surprises before a claim happens.

Quick Summary

- Many older North Texas homes still rely on original plumbing materials that naturally deteriorate over time.

- Tree roots commonly exploit aging sewer pipes, leading to backups that can damage the interior of a home.

- Home insurance usually does not pay to replace old or deteriorated plumbing systems.

- Water backup coverage can help pay for interior damage, but it is limited and optional.

- A full FAQ section is included at the end of this article for quick answers.

Why are plumbing problems common in older North Texas homes?

Plumbing problems are common in older North Texas homes because many were built decades ago using materials that were never meant to last forever.

Homes built between the 1940s and 1980s make up a large portion of the housing stock in Dallas–Fort Worth and surrounding areas. These homes are often built on concrete slabs, with plumbing systems buried underneath the foundation and out of sight.

Local factors that increase risk include:

- Aging pipe materials

- Expansive clay soil that shifts over time

- Mature trees with aggressive root systems

- Renovations that update surfaces but not infrastructure

What types of plumbing materials are found in older Texas homes?

Older Texas homes often contain plumbing materials that are now well past their expected lifespan.

Cast iron sewer pipes

Cast iron sewer pipes were commonly installed from the 1940s through the 1970s and typically last 40 to 70 years.

Over time, cast iron pipes can:

- Rust and scale from the inside

- Crack or separate at joints

- Allow roots to enter and expand

- Collapse without warning

Galvanized steel pipes

Galvanized steel water lines were widely used before the 1960s.

These pipes often experience:

- Internal corrosion

- Reduced water pressure

- Rust contamination

- Hidden leaks behind walls or under slabs

Orangeburg or fiber pipes

Some older homes still contain Orangeburg sewer lines, which were installed between the 1940s and early 1970s.

This material is especially failure-prone and can deform or collapse as it ages.

How do tree roots damage sewer lines in North Texas?

Tree roots damage sewer lines by exploiting small cracks or separations that already exist in aging pipes.

Roots are drawn to moisture escaping from deteriorating sewer lines. Once inside the pipe, they grow larger, trap debris, and restrict wastewater flow. Over time, this restriction can cause sewage to back up into the home through drains or toilets.

Roots rarely cause the original damage; they accelerate a failure that was already developing.

Why don’t standard home inspections catch sewer line problems?

Standard home inspections usually do not include sewer line camera inspections.

Most inspections focus on visible components and basic flow testing. Underground sewer lines are typically excluded unless a separate sewer scope is requested.

A sewer camera inspection can reveal:

- Cracks and joint separation

- Root intrusion

- Heavy corrosion

- Sagging or collapsed sections

For older homes, this inspection can uncover issues long before a backup occurs.

Does homeowners insurance cover old or failing plumbing in Texas?

Homeowners insurance usually does not cover old or failing plumbing caused by age, wear, or deterioration.

Most Texas policies exclude damage caused by:

- Wear and tear

- Corrosion

- Gradual deterioration

- Long-term root intrusion

Insurance is designed to cover sudden and accidental losses, not predictable aging of building systems.

The Texas Department of Insurance explains this distinction in their homeowners insurance and disaster claims FAQ.

What is water backup coverage and what does it pay for?

Water backup coverage is an optional endorsement that can help pay for interior damage caused by sewer or drain backups.

This coverage may apply when water backs up through:

- Drains

- Toilets

- Sewer lines

- Sump pumps (where applicable)

Important limitations include:

- Coverage is capped at a specific dollar amount

- Common limits range from $5,000 to $25,000

- Cleanup and mitigation costs count toward the limit

Without this endorsement, most sewer backup losses are not covered at all.

Why are plumbing repairs more expensive in slab homes?

Plumbing repairs are more expensive in slab homes because the pipes are buried beneath the concrete foundation.

Accessing failed plumbing may require:

- Jackhammering through floors

- Tunneling beneath the slab

- Structural and cosmetic repairs afterward

Even when interior water damage is covered, the cost to repair or replace the pipe itself is often excluded.

Common Misconceptions About Plumbing and Insurance

“If water damages my home, insurance will cover everything.”

Water damage coverage depends on the source and the endorsements on the policy.

“Roots caused the damage, so it should be covered.”

Insurance focuses on why the pipe failed, not what finished it off.

“A remodeled home has updated plumbing.”

Many renovations do not include sewer or water line replacement.

“Insurance will pay to replace the pipe if it backs up.”

Most policies pay for resulting damage, not aging infrastructure.

Real-World Claim Example: Sewer Backup in an Older North Texas Home

A homeowner experienced water coming up through multiple drains inside the house. The backup spread quickly, flooding much of the interior and damaging flooring, baseboards, drywall, and personal belongings.

The home was located in an older neighborhood and had an original cast iron sewer line beneath the slab.

The cause of the loss was root intrusion that had developed over time. Tree roots had entered the sewer line through separated joints and cracks caused by age-related deterioration of the cast iron pipe. As the roots expanded, they restricted flow until wastewater had nowhere to go but back into the home.

Because the homeowner had water backup coverage, the policy provided limited coverage for the resulting interior damage, including cleanup and repairs to affected areas of the home, up to the policy’s water backup limit.

However, the plumbing system itself was not covered. The damaged sewer line required replacement at the homeowner’s expense because the failure was caused by long-term deterioration and root intrusion — both of which fall under policy exclusions for wear, tear, and gradual damage.

In short:

- The backup event triggered coverage for interior damage

- The aging, deteriorated pipe that allowed the roots in was not covered

- Coverage applied only up to the water backup limit shown on the policy

Why This Claim Was Handled This Way

This outcome is consistent with most Texas homeowners policies and is one of the most common points of confusion for homeowners.

Here’s the key distinction your article should reinforce:

1. Cause vs. Resulting Damage

Insurance generally does not cover:

- Wear and tear

- Corrosion

- Deterioration

- Gradual root intrusion

But it may cover:

- Sudden water damage that results from a covered event or endorsement (like water backup)

In this case:

- Root intrusion and pipe separation developed over time → not covered

- Wastewater backing up into the home → covered only because of the endorsement

2. Why the Pipe Wasn’t Covered

Even though roots caused the blockage, the policy looks at why the pipe failed — not just what finished it off.

Root intrusion is typically viewed as:

- A consequence of existing cracks or joint separation

- A sign of aging infrastructure

- A maintenance-related issue, not a sudden accident

That’s why insurers pay for access and interior repairs (when endorsed), but not replacement of the sewer line itself.

3. Why Coverage Was Limited

Water backup coverage:

- Is optional

- Has a specific dollar limit

- Applies only to certain types of water damage

Cleanup alone can consume a large portion of that limit before repairs even begin — which is why many homeowners are surprised by how fast it’s exhausted.

Why This Scenario Is Worth Highlighting

This type of claim feels unfair to homeowners because:

- The damage is sudden and severe

- The plumbing failure feels catastrophic, not gradual

- The cost to fix the pipe often exceeds the insurance payout

But from a policy standpoint, the claim was handled exactly as written.

That’s the educational value of this story:

Insurance didn’t fail — expectations were just misaligned.

What Could Have Changed the Outcome?

There was no single mistake in this scenario — but there were a few decisions and realities that shaped how much financial help was available when the loss happened.

1. Higher Water Backup Coverage Limits

The homeowner did have water backup coverage, which made a major difference. Without it, none of the interior damage would have been covered.

That said, many policies default to relatively low limits. Cleanup, drying, and mitigation alone can consume a large portion of that coverage before repairs even begin.

What could have helped:

- Higher water backup limits (when available)

- Reviewing limits based on home age and plumbing type

- Understanding that backup coverage is often exhausted faster than expected

2. Knowing the Plumbing Was Near the End of Its Life

Cast iron sewer lines commonly reach the end of their useful life after several decades. In older homes, deterioration often happens out of sight, under the slab, until a failure forces attention.

What could have helped:

- Awareness of the home’s original plumbing materials

- Proactive planning for eventual replacement

- Budgeting for infrastructure updates separate from insurance expectations

Insurance generally responds to sudden losses — not predictable aging.

3. A Sewer Line Camera Inspection Before the Loss

Sewer line issues almost always develop over time. A camera scope can reveal:

- Cracks and separations

- Heavy scaling

- Root intrusion

- Partial collapses

What could have helped:

- A sewer scope during purchase

- Periodic inspections in older homes

- Identifying problems before they turned into an interior loss

This doesn’t change what insurance covers — but it can prevent the loss entirely.

4. Understanding What Insurance Is (and Isn’t) Designed to Do

One of the hardest parts of claims like this is emotional, not contractual.

Insurance is not a home warranty and not a maintenance plan. It’s designed to help with sudden, accidental damage, not the cost of replacing aging systems.

What could have helped:

- Clear expectations before a loss

- A coverage review focused on worst-case scenarios

- Knowing which risks remain the homeowner’s responsibility

5. Reviewing Coverage Before Something Goes Wrong

Most homeowners review coverage only after a loss — when it’s already too late to change anything.

What could have helped:

- A proactive policy review

- Adjusting endorsements as the home aged

- Asking “How would this actually be paid if it happened?”

Sometimes the most valuable outcome of a coverage review is knowing what won’t be covered, not just what will.

The Big Takeaway

In this scenario, insurance worked exactly as written — but different choices and awareness could have reduced the financial impact.

The goal isn’t to eliminate risk entirely. It’s to avoid surprises when the stakes are highest.

FAQ: Old Plumbing, Sewer Backups, and Cast Iron Pipes in North Texas Homes

These answers are general guidance. Coverage depends on the policy wording, endorsements, and the cause of loss.

Is cast iron plumbing covered by homeowners insurance in Texas?

Cast iron plumbing is usually not covered when it fails due to age, corrosion, deterioration, or long-term wear.

Does water backup coverage cover sewer backups in Texas?

Water backup coverage can help pay for interior damage when water comes up through drains or toilets, but it is typically optional and subject to a specific limit.

Does water backup coverage pay to replace the sewer line?

Water backup coverage typically helps with damage inside the home and does not pay to replace a deteriorated sewer line or plumbing system.

How much water backup coverage should I have for an older home in DFW?

Older homes in Dallas–Fort Worth often benefit from higher water backup limits when available because repairs to flooring, drywall, and contents can exceed lower limits quickly.

Are sewer camera inspections worth it for older homes in North Texas?

Sewer camera inspections are often one of the most valuable add-on inspections for older North Texas homes because they can identify root intrusion, cracks, and deterioration before a major backup happens.

What happens if roots damage my sewer line and it backs up into my house?

If roots contributed to a long-term pipe failure, the sewer line itself is often not covered, but interior damage may be covered when water backup coverage is included and subject to the endorsement limit.

What warning signs suggest a deteriorating sewer line in an older Texas home?

Common warning signs include recurring slow drains, frequent clogs, gurgling sounds, sewer odors, or backups that affect multiple drains at the same time.

Article Summary

Older North Texas homes often contain aging plumbing systems that fail gradually and unexpectedly. Insurance usually does not pay to replace deteriorated pipes, but water backup coverage can help with limited interior damage. Understanding plumbing materials, inspection options, and coverage limits before a loss can prevent costly surprises later.

Not Sure If a Sewer Backup Would Be Covered in Your Texas Home?

Many policies handle drain and sewer backups differently than other water damage, and coverage is often limited unless a specific endorsement is in place. A quick policy check can help you confirm whether you have water backup coverage and what the limit is.

Related Articles

- Home Guide

- ACV vs RCV Roof Coverage in Texas: What Homeowners Actually Get Paid

- Flood Insurance in Texas – Essential Facts

- Does Home Insurance Cover Roof Leaks in Texas?

- What Isn’t Covered by Home Insurance in Texas (2026 Guide)

Luke Faulkner is a Texas-licensed insurance advisor and the founder of Gilded Oak Insurance. He helps Texas drivers and homeowners make confident coverage decisions through clear, practical guidance — without pressure or fear-based selling.

Learn more about our mission and approach on the Gilded Oak Insurance About page .

⚜️ Stay Connected with Gilded Oak

Join us on social for insurance savings tips, light-hearted entertainment, and everyday insights that make coverage easier (and a little more fun) to understand.

Request a Quote